ALEJANDRO JIMENEZ: Solving Small Companies' Private Debt Challenge

Europe and Estonia are lagging the U.S. in private debt funding with a wide margin

Private debt is a privately negotiated loan between a non-bank lender and a company.

Europe is lagging badly in this space.

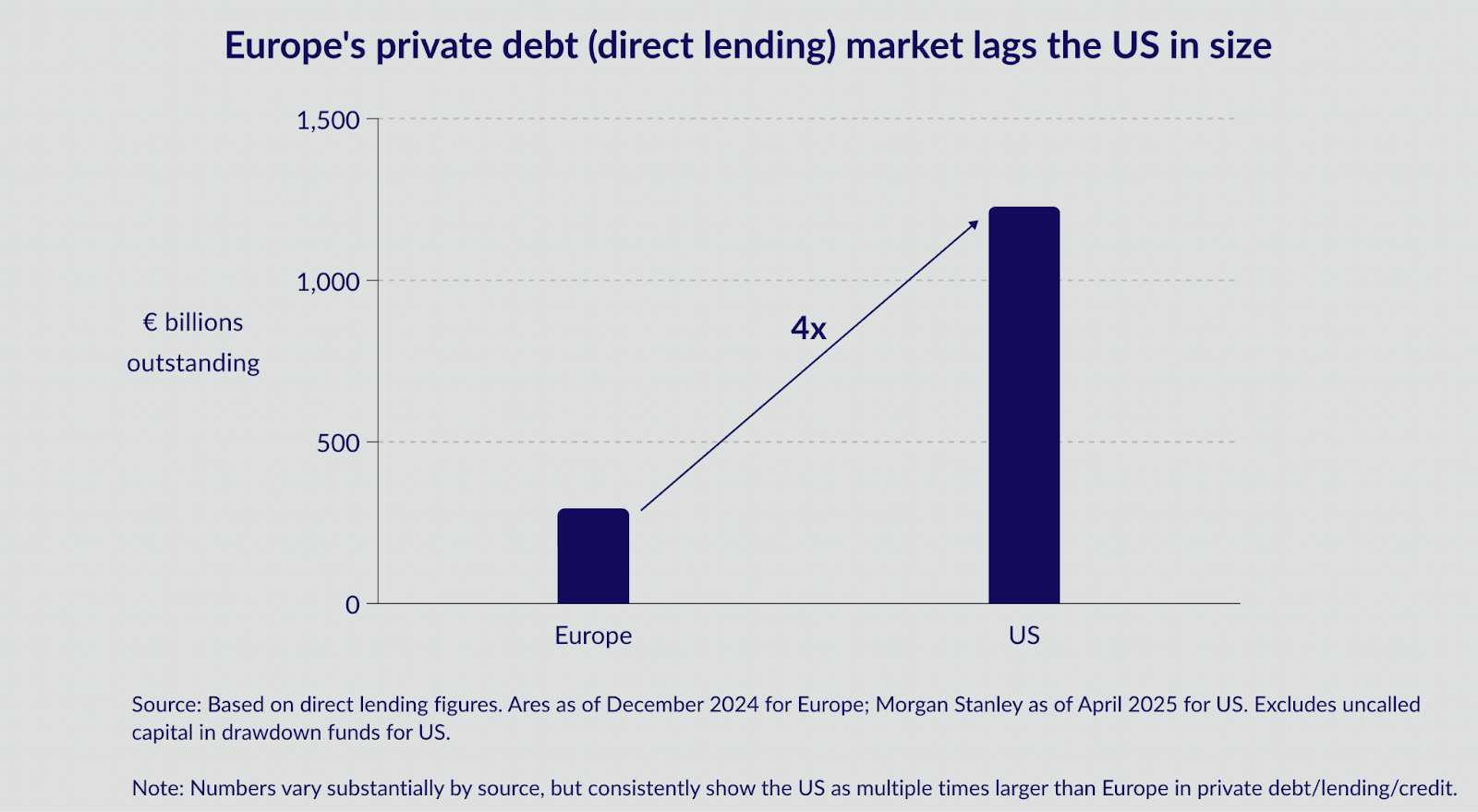

The US private market for direct lending to companies is $1.4 trillion (€1.2tn), yet Europe’s is only €294 billion. An enormous 4x difference for two economies of similar size.

Even when including bank loans and bond markets alongside private debt, European companies still receive less capital than their American counterparts, both in absolute terms and relative to GDP.

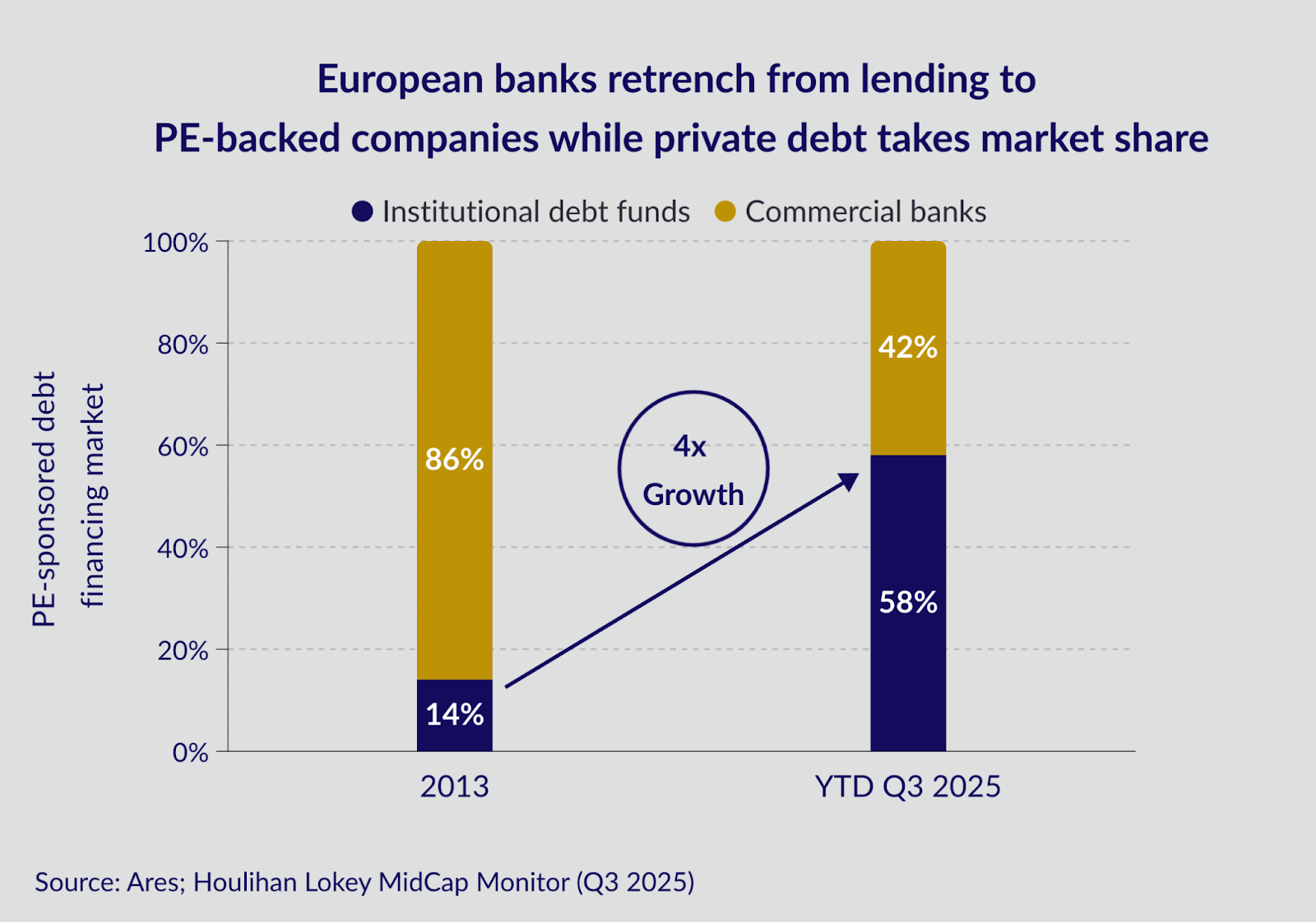

Heavy regulation after the 2008 financial crisis has limited the amounts banks can lend. One area notably affected is bank lending to private equity-owned companies. Consequently, private debt has stepped in to take a large share of these loans. But more is needed.

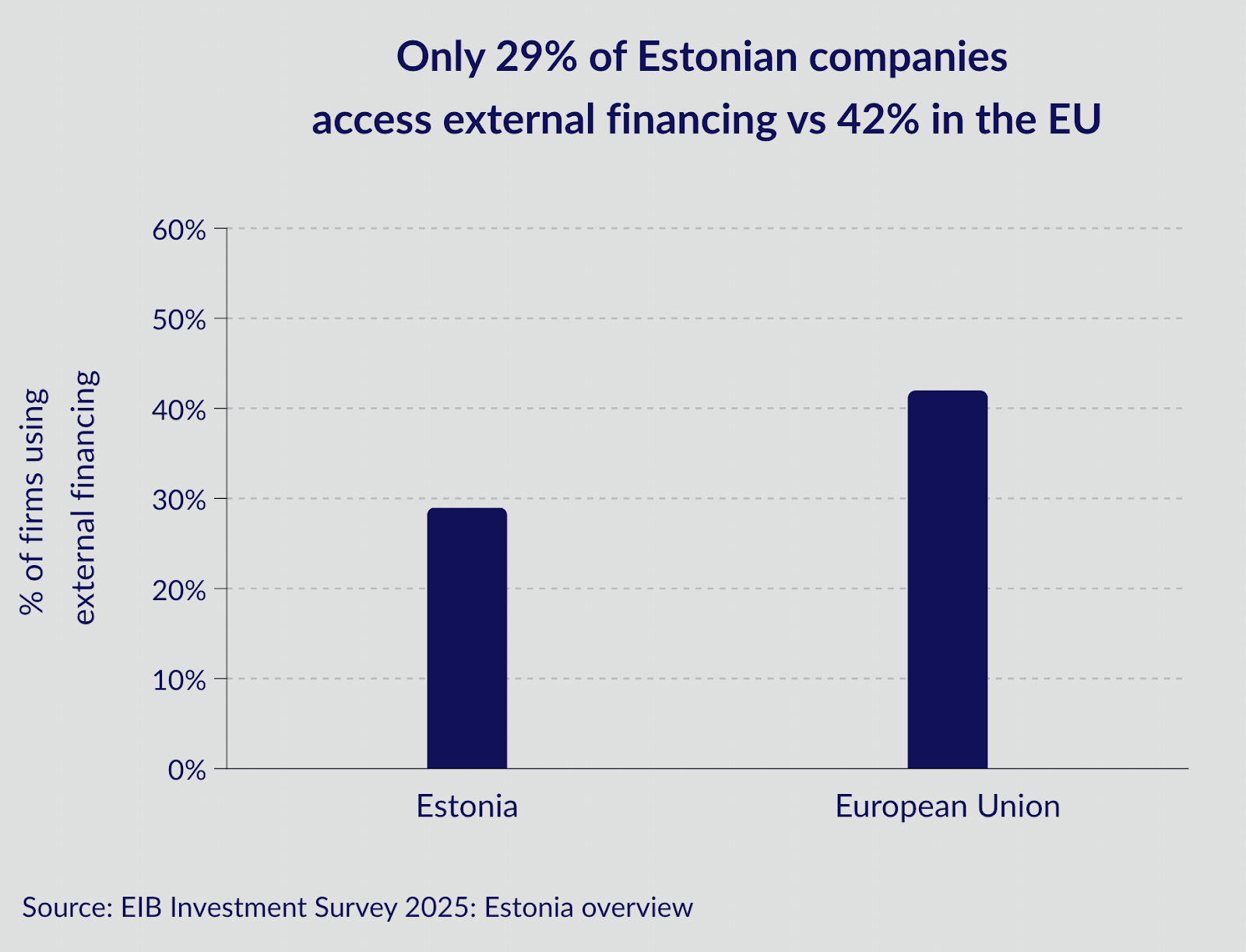

In Estonia, the problem is even worse

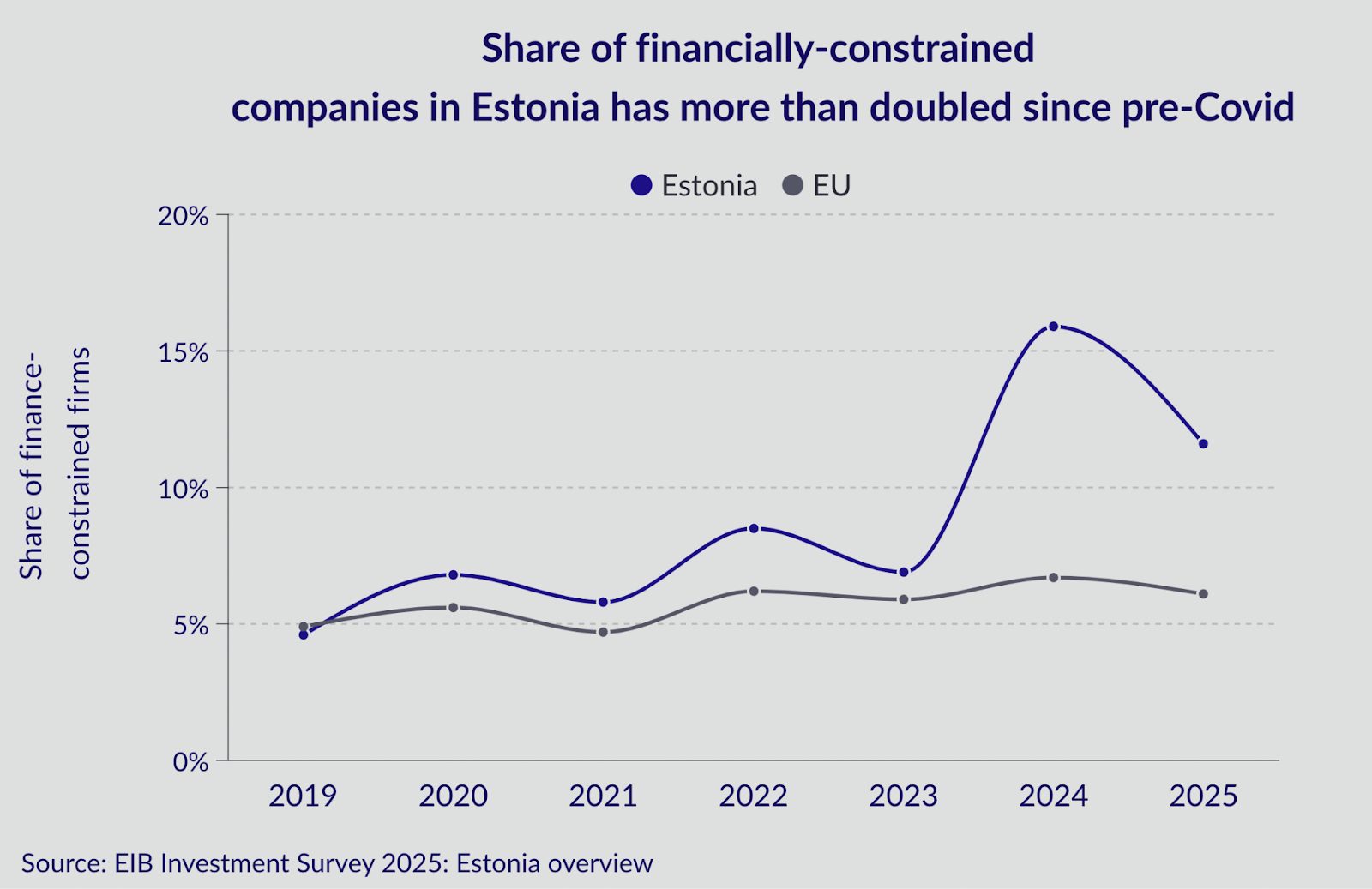

Only 29% of Estonian companies access loans or the capital markets to finance their investment needs, significantly below the EU’s 42%, according to the EIB. Meanwhile, the share of financially-constrained companies in Estonia has more than doubled to 12% since pre-COVID, again worse than in the EU.

To solve the problem, I founded TriHeritage Global Capital, a private debt firm offering loans to profitable small businesses and scaleups in the EU. We offer up to €1 million per loan, but expect to increase this amount if we can grow successfully together.

What is the lending model of private debt?

Private debt firms can either offer loans as a standalone product or co-offer capital alongside a private equity (PE) or venture capital (VC) fund.

In the standalone scenario, the private debt firm simply provides a loan to the borrowing company.

In the co-offering scenario, the borrowing company receives a loan from the private debt firm and equity from a PE/VC firm, increasing the total capital received (like the classic leveraged buyout (LBO), through which shareholders amplify their return on equity by adding debt). Existing shareholders will experience ownership dilution, though less than if the entire capital comes exclusively from PE/VC.

In the US, where co-offerings are common, private debt firms typically provide $1 in loans for every $5 in equity from the PE, resulting in a $6 capital injection for the borrower.

At TriHeritage, we can provide loans as both a standalone and co-offering.

What is the interest rate on private debt?

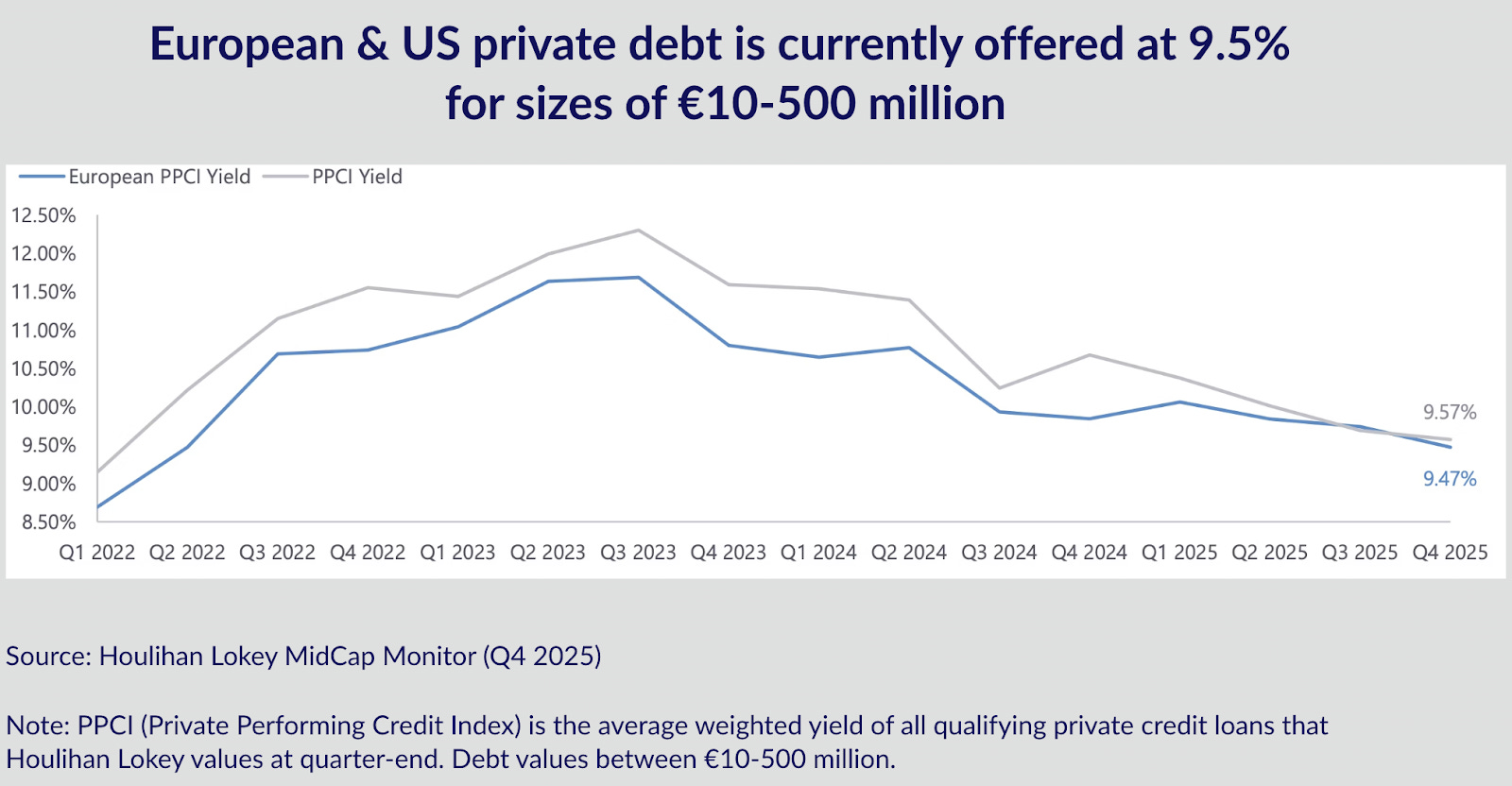

Data is scarce for small deals, but an index of private loans sized €10-500 million shows a rate of 9.5%.

Of course, this rate varies based on each company’s strength, size, geography, industry, and overall risk.

For small businesses and scaleups

To set clear expectations, at TriHeritage we focus on small businesses and scaleups that offer a product/service with proven viability, positive operating profits, and a kick-ass management team.

We are not an early-stage VC or Angel risking capital in exchange for sky-high returns. Our return is capped at the interest rate, so we will not take disproportional risk by investing in early stages.

We work with the next stage of a company’s evolution and expect loan repayment, which requires the borrower to have sufficient cash flow.

Points to consider by the borrowing company

Debt financing, used responsibly, can provide companies with growth capital for initiatives such as new market entry, M&A, factory expansion, new services, hiring talent, and upgrading technology.

Debt financing is non-dilutive to shareholders when offered on a standalone basis.

However, a portion of operating profits will be used for interest payments, which may reduce profits if the company doesn’t grow. The company also needs a credible growth strategy to generate sufficient capital to repay the loan.

Did Silicon Valley Bank offer something similar?

Silicon Valley Bank (SVB) offered loans and co-invested capital along with VCs. That’s as far as the similarities go.

SVB was a bank, not an investment firm.

SVB succumbed to a classic bank run, triggered not by faulty loans—its loan portfolio was pretty healthy—but by a fatal duration mismatch. The bank accepted deposits, which depositors could withdraw daily, and it mistakenly reinvested these into long-term bonds.

Depositors started demanding money back, while the value of SVB’s bond holdings had coincidentally fallen. Depositors perceived that SVB could no longer cover its obligations to them, quickly leading to a bank run and bankruptcy.

The core issue was SVB’s mismatch between its short-term liabilities (deposits) and long-term assets (bond holdings).

This mismatch is also affecting some US private credit funds that promised their investors daily liquidity to fund long-term loans.

TriHeritage is not a bank, and we don’t take deposits. Our money is longer-term, like the loans we offer.

----------------

Alejandro Jimenez is Co-founder & Managing Partner at TriHeritage Global Capital, an Estonia-based firm providing loans to profitable small and midsize companies across the EU. Loans are customised with a floating interest rate and a 3-year maturity, not diluting shareholders.

Previously, Alejandro was a partner in New York and Geneva at J.P. Morgan, the world’s largest financial institution. He also ran the energy trading desk at Enefit and managed sustainable investment portfolios at Grunfin.