ALEJANDRO JIMENEZ: "But he started it!"

The economic fallout from the Iran war is more severe for Europe than for the US

“But he started it!” is a common cry from my kids whenever I intervene to break up a scuffle. Europe can point to Donald Trump and say the same about his incursion into Iran, a war that affects Europe far worse economically than it does the US, “but he started it!”

European leaders weren’t even consulted ahead of the American-Israeli joint attack on Iran that began this February, and which has rattled energy markets.

Oil and gas remain the engines of the global economy, with much of it coming from the Middle East. Major producers such as Saudi Arabia, Qatar, Iraq, and Iran export oil and gas via the Strait of Hormuz. It’s the only sea passage from the Persian Gulf to the open ocean.

Around 20% of the world’s oil and liquefied natural gas (LNG) passes through the Strait.

Since the war began, Iran has blocked passage of ships through the Strait, which at its narrowest point is only 33 km wide. Closing the Strait is illegal under international law, but because of Iran’s coastal position, it can easily choke the flow of ships with threats of missiles and underwater mines. Shipowners, naturally, are not risking their tankers’ destruction or the lives of crews. The region’s oil and gas are stuck with few options.

Oil prices have risen by over 50% in Europe and the US since the outbreak of the war.

Natural gas prices are up a whopping 70% in Europe. However, natural gas prices in the US are actually down 1%. More on this in a moment.

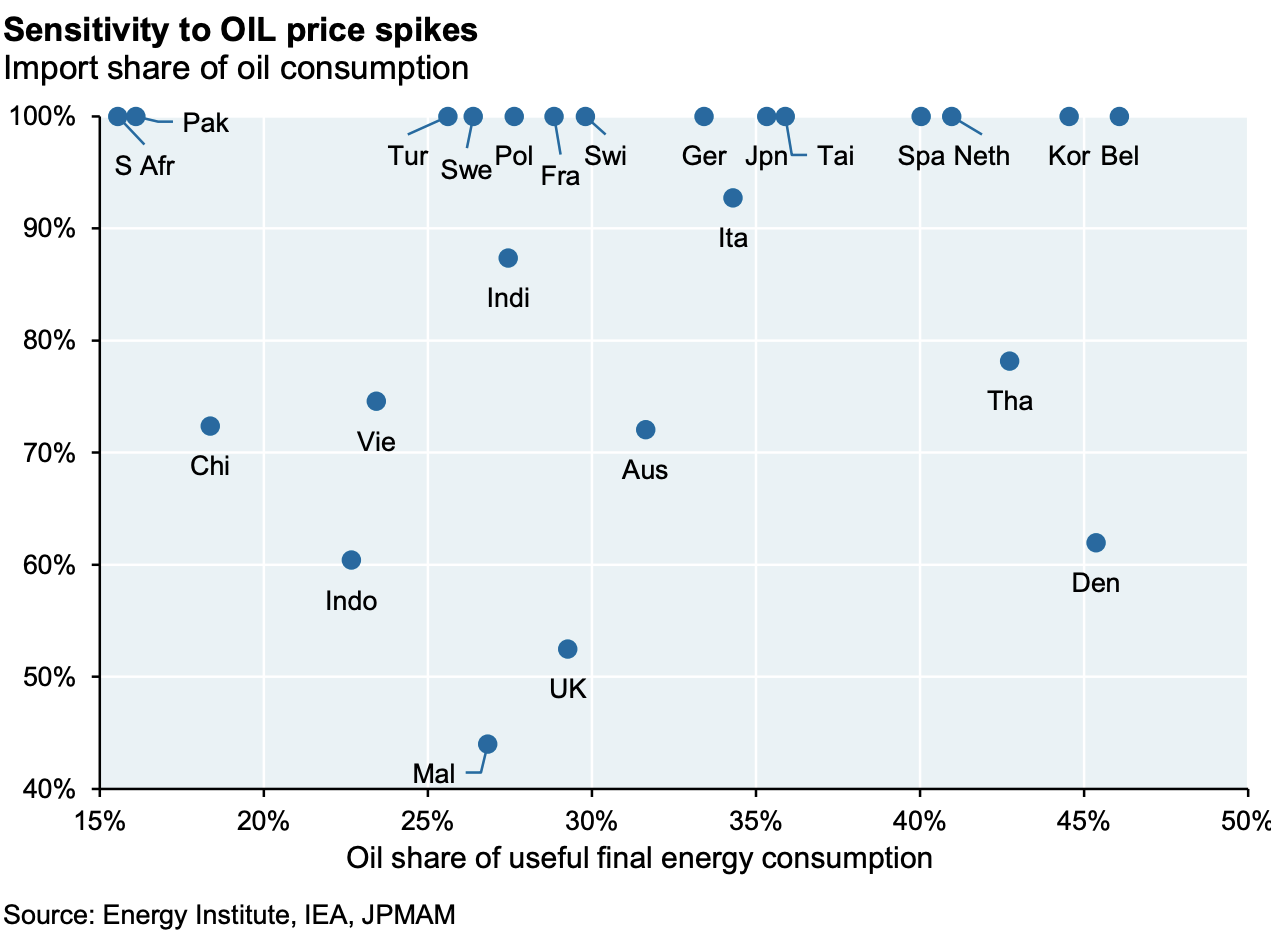

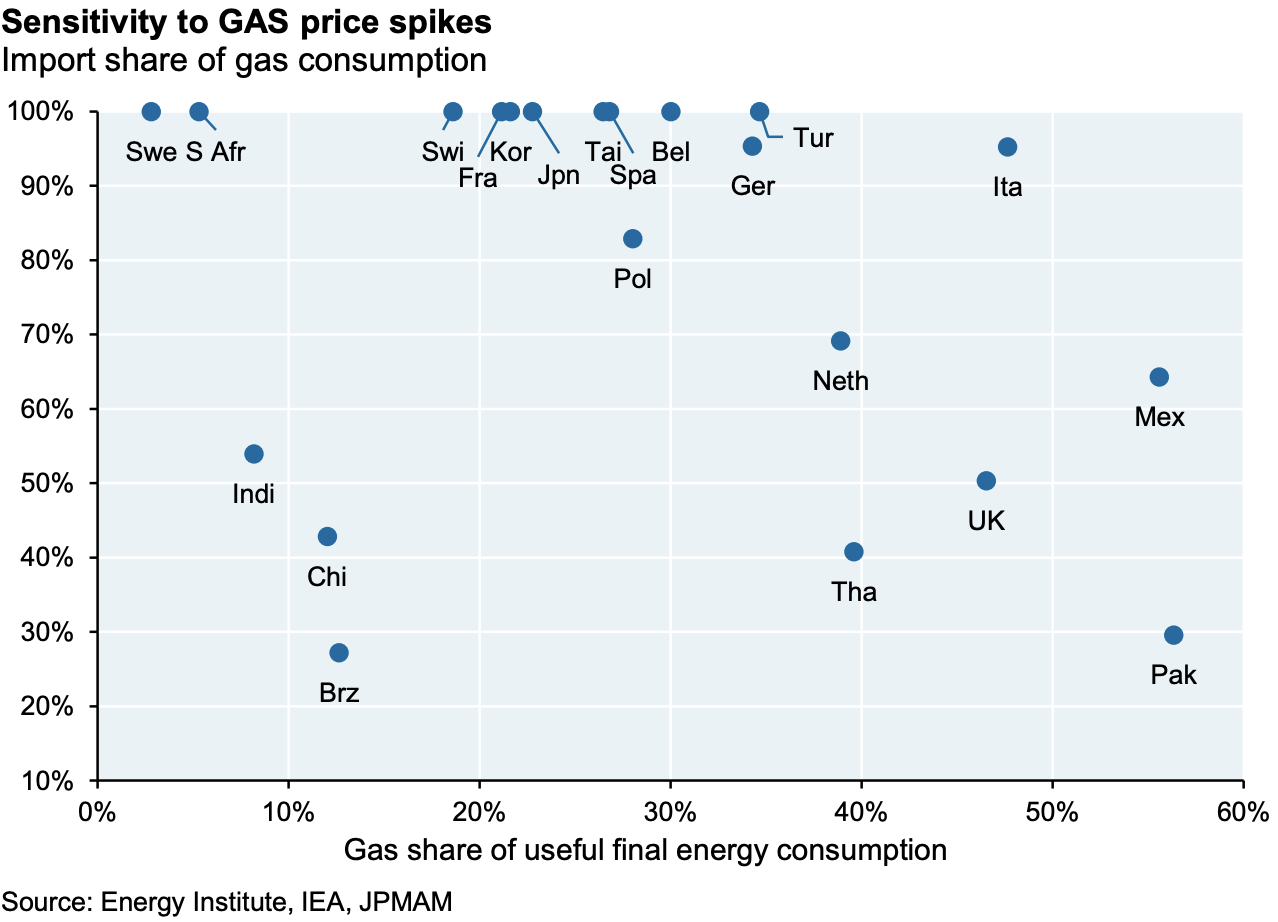

Spain, Italy, Germany, and Belgium are highly dependent on oil and gas in their total energy consumption. To make matters worse, they import almost all of it.

In other words, Europe is highly exposed to the risks of both high prices and supply shocks.

Check out these two charts from JP Morgan. One chart shows a country’s use of oil as a share of its total energy consumption (x-axis) and how much of that oil is imported (y-axis). The other chart does the same, but for gas.

The most vulnerable countries are towards the upper right.

Don’t be fooled by all the social media posts celebrating Spain’s energy independence, driven by its extensive green electricity. These posts are incomplete. Electricity is just one portion of total energy consumption. While Spain’s electricity is indeed mostly green, the majority of the country’s overall energy consumption, which includes transportation, heating, and manufacturing, still relies heavily on oil and gas. Therefore, Spain’s total energy consumption is still 65% reliant on oil and gas, both of which are imported. A far cry from energy independence.

The US, conversely, is a net exporter of oil and gas. And, as mentioned earlier, US natural gas prices are down 1% since the war began. The US produces its own gas and consumes it locally, making the nation less vulnerable to supply shocks. In fact, most gas across the world is consumed where it’s produced, making prices local. LNG, the gas shipped globally after a complex process of liquefaction, is only 14% of the world’s gas. As Europe isn’t a major gas producer, it needs to import LNG at higher global prices.

If the war persists, inflation could again become a problem in Europe. Oil and gas are major cost components in manufacturing, transportation, heating, plastics for medical supplies, and fertilizers for food, all of which push up the final price of goods. Oil and gas also feed into higher electricity prices on cloudy and windless days when there’s no solar or wind energy production (see my Fomo.Observer article from Feb 9 on how electricity prices are set).

Europe’s economic growth has lagged the US for years, with giant Germany stuck in a rut for the last three. The US’s cheaper natural gas will make it even more cost-competitive vs Europe.

Once the war ends, Europe might be stuck with higher permanent costs. Iran may apply tolls to all ships crossing the Strait going forward. A 10% toll on the total cargo value has been discussed, a cost the final consumer would likely bear.

There’s a common saying, “a war is ‘easy’ to start but very difficult to end”, and it’s not clear where this conflict goes from here.

Iran and Israel’s fight is existential, meaning they can withstand a longer and more painful war than the West. The US’s goal, although not fully clear, is definitely not about survival. The objectives of Israel and the US are misaligned. The US has likely lost control of this war, even if it declares “victory” and exits the conflict on the basis of some vaguely defined achievement. Iran and Israel will ultimately decide how this war ends.

Despite the US’s stronger energy position, Trump is not immune. Unlike natural gas, oil prices are global. Oil can be shipped around the world and sold to the highest-paying global buyer. Around 75% of global oil trade is maritime compared with just 14% for natural gas. Consequently, this affects petrol prices for US drivers. Americans love their big, petrol-guzzling cars. Therefore, high prices at the pump could make voters turn against Trump’s Republican Party ahead of November’s midterm elections. Trump is keenly aware of this, and his tolerance for a long war is low.

If the US exits the war and leaves Europe to deal with the mess, Europe can emphatically say, “But he started it!”

P.S. Geopolitical events underscore the vital importance of predictable business costs to stay competitive. If your company is uncomfortably exposed to gas, electricity, or oil prices, a long-term hedging strategy could help reduce cash flow volatility. At TriHeritage we offer advisory services and can help you plan a strategy. Reach out to me.

----------------

Alejandro Jimenez is Co-founder & Managing Partner at TriHeritage Global Capital, an Estonia-based firm providing loans to small and midsize companies across the EU. Previously, Alejandro was a partner in New York and Geneva at J.P. Morgan, the world’s largest financial institution. He also ran the energy trading desk at Enefit and managed sustainable investment portfolios at Grunfin.